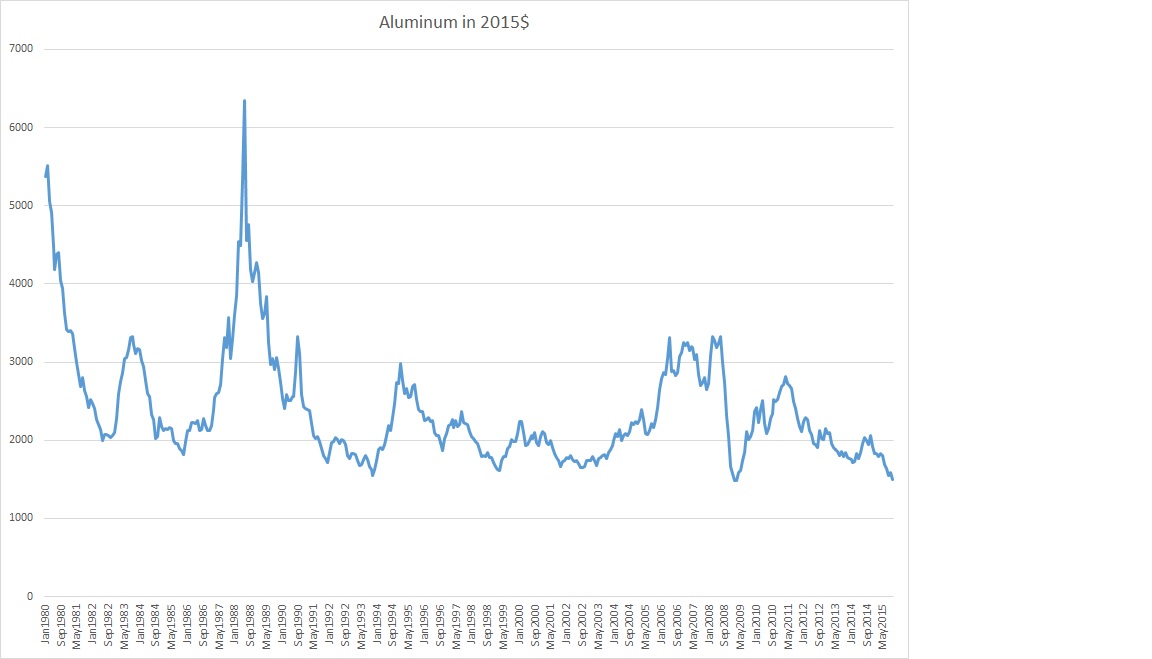

....is Aluminum! Here's a long term graph of the price in 2015$:

So aluminum is just about at all time record lows!

Now there is a good reason for this. In a word, China. The Chinese investment bubble of the past 20 years was truly incredible, on the order of the Japanese property bubble of the 1980s. A lot of the overbuilding went into capital intensive areas, like aluminum smelters. Additionally, there was huge overbuilding in construction and infrastructure, areas that use a fair bit of aluminum. So when China started decelerating last year, there was both an increase in supply and a decrease in demand.

Here's a graph of aluminum production that shows the Chinese effect very clearly. The data is only through Jan of 2015, but I understand that the trend has continued. Note how Chinese production has accelerated as ROW production slightly declined:

To my mind, the oversupply will last quite awhile. The Chinese are not likely to reduce production. In fact there are some new smelters due to come onstream in western China. The large state owned industries in China make production decisions on noneconomic issues, like keeping people employed and hitting the Party's targets. They probably won't be starting any new capacity additions, but it will take a long time to work out the existing amount. In the meantime the state owned banks will extend credit to cover their losses.

Longer term, the outlook is not that bad. Aluminum is heavily used in aerospace and is increasingly used in automobiles and trucks. These are growth areas. It is also used in general infrastructure, which will probably continue to grow moderately. So the issue is how long till the excess supply gets worked off. Alcoa has said publically that it expects its aluminum demand to grow by 7% per year. This may be overoptimistic for the industry as a whole; Alcoa serves the fast growing aerospace and automotive industries. Nonetheless, this is going to take awhile.

So how and if should one invest in this. The simplest way would be to buy aluminum metal and store it. Off LME exchange carrying costs are quite low. If aluminum can get back to its long term deflated average in five years, it will give a return of just under 10% per year. To my mind, that's not worth the risk.

Another way would be to invest in a western aluminum company that is likely to survive the low prices and emerge profitable when they go back up. Alcoa is an obvious candidate here. Its downstream business is quite profitable and is going to be spun off later in the year. Note though that this is more of a play on the fabricating and casting business than a pure commodity play.

In times of low prices, I always think it's best to buy the low cost producer. The lowest cost publicly traded producer is probably Rio Tinto, but aluminum is not a majority of their business. Behind it comes Rusal (Russian) and Norsk Hydro (Norwegian), which are more pure plays. If you are willing to take the Russian political and governance risks, I would go for Rusal.

I have a very small position in Alcoa preferred. I would add the common stock if got into the low 8s.