In Jan 2018, I published a post in Seeking Alpha explaining why I was bullish on Vanadium. I recommended two stocks, Largo Resources and Advanced Metallurgical Group. The timing on the recommendation was just about perfect. Vanadium pentoxide skyrocked from about $8 / lb. to eventually over $35. Later in the year I wrote another piece that was decidedly less bullish. I wound up makeing good money on the trade, although I scaled out far too soon. It would have been a home run, but such is life.

I'm now back in. The V2O5 price fell to about $7. This was a blow off bottom in my view. This time I'm concentrating on Largo. It's not a perfect company, but it is a pure play, and it will soon be debt-free. I scaled in from C$ 1.75 to C$1.6. So we will see.

Thursday, June 13, 2019

Saturday, May 25, 2019

Cobalt Part Two

The last post put Cobalt into a general value area. Now let's look at the supply/demand. This is tricky since it depends on a forecast of electric vehicle demand. Here's my best estimate. Just remember that this is subject to wide ranges.

'000 tonnes of refined metal equivalent

'000 tonnes of refined metal equivalent

So there's about 24 K tonnes that has to be satisfied by new mines or additional recycling that have not yet been committed. I think that this can be done without a major price rise. OTOH, it's hard to see the price go down much unless there is a change in the EV outlook. If it did, the necessary new supply would evaporate.

My best guess is that Cobalt will move in a wide band for the next few years, with no major bull or bear market. We are probably near the bottom of the range.

Tuesday, May 21, 2019

More on Battery Metals

This is the second in a series of posts about battery metals. By battery metals I mean:

Lithium

Cobalt

Graphite

Nickel

This post will be about cobalt (Co).

The bull argument was that increased demand from electric cars and grid storage systems would raise demand for all these metals to a new plateau. There is actually some truth to the argument. Previously, all these metals were used in other applications. Cobalt and lithium are used primarily in the chemical industry, nickel in steel. The new source of demand should force producers to go out further on the cost curve.

But everything has its limits. The above narrative soon became a mania, with the usual suspects (retail, southwestern family offices) piling in. In cobalt,there is even a streaming company, Cobalt27. Nothing attracts retail like streaming.

There are a lot of counter movements.

- Technological improvement. Volkswagen plans to reduce the Co content of its EV batteries from the current 12% to 4%. Li ion batteries are a relatively new technology. There's plenty of improvement yet to be made. It's true that the basic science is known, but there are a lot of improvements that can be made incrementally.

- Recycling. Right now very few Li ion batteries get recycled. That is obviously not a long term solution. The whole point of EVs is environmental, so why create a poisonous landfill problem? This matters to the kind of person who will buy an EV and to the regulators who set the rules. I have seen estimates that 20% of Co demand will be covered by recycling by 2030.

- New mines. Right now the Democratic Republic of the Congo (DRC) is by far the world's largest supplier. I can't think of a less stable source of supply. But Co isn't that rare. New mines are being considered in Australia and the US. These are probably only marginally economic at current prices, but might be worthwhile for security reasons.

OK, enough generalizations. Let's get specific about cobalt. I'm starting with this because I feel it has the best bull case and it's investible.

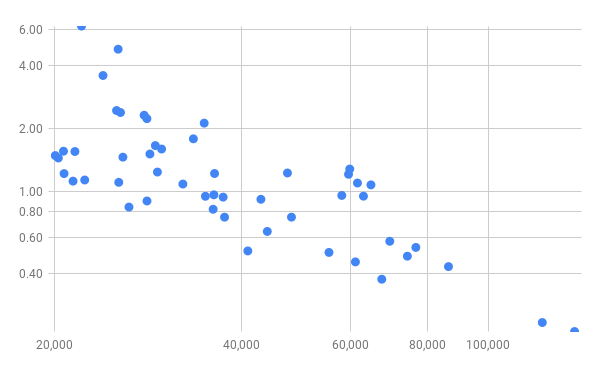

When looking at any new commodity investment, I always start with long term value. Here's a graph I like to use (BTW, I keep these graphs for about 200 commodities.)

For those of you who haven't seen this type of chart before:

For those of you who haven't seen this type of chart before:

- The X-axis is the real price of vanadium (inflation and currency adjusted) $ /tonne.

- The Y-axis is the 10-year forward price appreciation/depreciation in inflation adjusted dollars.

Right now, the price is about $34,000. So the graph is forecasting about a 20% real price appreciation in the next ten years. That's 1.8% per year, not good enough to cover cost of carry.

But what about the argument that the new source of demand will push Co production out the cost curve? For that we have to build a supply/demand model.

Gotta run. More later today or tomorrow...

Lithium

Cobalt

Graphite

Nickel

This post will be about cobalt (Co).

The bull argument was that increased demand from electric cars and grid storage systems would raise demand for all these metals to a new plateau. There is actually some truth to the argument. Previously, all these metals were used in other applications. Cobalt and lithium are used primarily in the chemical industry, nickel in steel. The new source of demand should force producers to go out further on the cost curve.

But everything has its limits. The above narrative soon became a mania, with the usual suspects (retail, southwestern family offices) piling in. In cobalt,there is even a streaming company, Cobalt27. Nothing attracts retail like streaming.

There are a lot of counter movements.

- Technological improvement. Volkswagen plans to reduce the Co content of its EV batteries from the current 12% to 4%. Li ion batteries are a relatively new technology. There's plenty of improvement yet to be made. It's true that the basic science is known, but there are a lot of improvements that can be made incrementally.

- Recycling. Right now very few Li ion batteries get recycled. That is obviously not a long term solution. The whole point of EVs is environmental, so why create a poisonous landfill problem? This matters to the kind of person who will buy an EV and to the regulators who set the rules. I have seen estimates that 20% of Co demand will be covered by recycling by 2030.

- New mines. Right now the Democratic Republic of the Congo (DRC) is by far the world's largest supplier. I can't think of a less stable source of supply. But Co isn't that rare. New mines are being considered in Australia and the US. These are probably only marginally economic at current prices, but might be worthwhile for security reasons.

OK, enough generalizations. Let's get specific about cobalt. I'm starting with this because I feel it has the best bull case and it's investible.

When looking at any new commodity investment, I always start with long term value. Here's a graph I like to use (BTW, I keep these graphs for about 200 commodities.)

- The X-axis is the real price of vanadium (inflation and currency adjusted) $ /tonne.

- The Y-axis is the 10-year forward price appreciation/depreciation in inflation adjusted dollars.

Right now, the price is about $34,000. So the graph is forecasting about a 20% real price appreciation in the next ten years. That's 1.8% per year, not good enough to cover cost of carry.

But what about the argument that the new source of demand will push Co production out the cost curve? For that we have to build a supply/demand model.

Gotta run. More later today or tomorrow...

Wednesday, May 15, 2019

New article on Seeking Alpha

I just posted an article on Seeking Alpha, https://seekingalpha.com/article/4264315-new-chinese-tariffs-looking-numbers

I believe it's free for everybody for now.

I believe it's free for everybody for now.

Tuesday, May 14, 2019

The Bust in Battery Metals

When markets go into bubble mode, the bust is often worse than you thought possible. Often, the reason is that during the bubble, speculative stocks of the commodity get built up. In some commodities, these stocks may not be visible. They may be the result of producers accumulating inventory or work in process, or consumers accumulating inventory. When the bust comes, it may take quite awhile for these stocks to be liquidated.

This is the story in "battery metals", a group that includes lithium, cobalt, graphite and some others.

Now that we are in the down cycle, let's look at whether there is a long term opportunity here.

I am going to write a series of posts on this. At the end, I'll put it into an article that I'll publish on one of the large financial websites.

For now, here's a graph of cobalt deflated to 2019$. As usual I am using the PCE deflator. I am also adjusting the price for the value of the $US against a broad index of other currencies. You can see that the price has declined to a reasonable, but not dead cheap, level.

This is the story in "battery metals", a group that includes lithium, cobalt, graphite and some others.

Now that we are in the down cycle, let's look at whether there is a long term opportunity here.

I am going to write a series of posts on this. At the end, I'll put it into an article that I'll publish on one of the large financial websites.

For now, here's a graph of cobalt deflated to 2019$. As usual I am using the PCE deflator. I am also adjusting the price for the value of the $US against a broad index of other currencies. You can see that the price has declined to a reasonable, but not dead cheap, level.

Thursday, May 9, 2019

An Aside: How to Negotiate

I have no inside information on what is going on with the China trade deal. I only know what I read on the screen. Here's a personal story that may be relevant.

When I was younger I sold my first house. The buyer was antsy, and it was hard to come up with a price both sides could live with. We finally did, and met to sign the deal. At the signing, the buyer came up with another demand. He told me that after relooking at the house, he wanted a discount for some issue (forgot what it was). Since he had previously had an engineer go over it, this seemed pretty fishy.

My father said that this was a typical although somewhat sleezy negotiating tactic. One side figures the other has become psychologically invested in the deal, and will be willing to give a little more to get it done. He recommended I say no. I did. A couple of days later we signed the deal. I gave him a very small discount (I think about 0.1%) to sooth his ego. In return part of his down payment was made non-refundable, to sooth mine. The deal went through smoothly.

Sound familiar?

When I was younger I sold my first house. The buyer was antsy, and it was hard to come up with a price both sides could live with. We finally did, and met to sign the deal. At the signing, the buyer came up with another demand. He told me that after relooking at the house, he wanted a discount for some issue (forgot what it was). Since he had previously had an engineer go over it, this seemed pretty fishy.

My father said that this was a typical although somewhat sleezy negotiating tactic. One side figures the other has become psychologically invested in the deal, and will be willing to give a little more to get it done. He recommended I say no. I did. A couple of days later we signed the deal. I gave him a very small discount (I think about 0.1%) to sooth his ego. In return part of his down payment was made non-refundable, to sooth mine. The deal went through smoothly.

Sound familiar?

Tuesday, May 7, 2019

China deal off? What comes next.

Well. I guess I was wrong. I had thought the US-China trade deal was going to happen. It was always in the interest of the US, and I thought it was likely in China's interest as well. But I suppose asking China to change what had been a successful economic strategy for 40 years is asking too much.

There's of course still a chance that a deal can be reached. But if not, here's what I see will happen...

- Over the short term, the increased tariffs will largely be paid by the Chinese private sector. These factories really have no where else to sell their output, so their prices will go down. Some of it will be paid by US consumers, but not much. US companies (and other multinationals) that have established worldwide supply chains in China will suffer, as these factories are now stranded assets. There is a lot of this, so it is negative for the stock prices of these companies and thus the market as a whole.

- Longer term, supply chains will be relocated to other emerging Asia. So it's actually bullish for some assets in these countries, like real estate. Banks in places like Indonesia, Vietnam etc. would also benefit. I want to stress that this is longer term stuff. Shorter term, assets in EM will suffer, with the risk of a blowup in highly stressed ones like Turkey or Argentina.

- The next trade domino will be the EU. Since that area is already in secular stagnation, this could have serious consequences. A lot of the EU stock market is auto-based, and this would be the main target. If the Germans allow a fiscal stimulus, this could be managed. Don't bet on it.

The most important trading advice I can give is not to trade on stuff you don't have a strong view about. I felt that the deal was going to go through, but I knew I didn't have any insight that the market didn't already know. So I did not trade it. If I had shorted bonds, like I was thinking about a few posts ago https://thecommoditystrategist.blogspot.com/2019/04/long-time-no-post.html, I would already be out of pocket.

There's of course still a chance that a deal can be reached. But if not, here's what I see will happen...

- Over the short term, the increased tariffs will largely be paid by the Chinese private sector. These factories really have no where else to sell their output, so their prices will go down. Some of it will be paid by US consumers, but not much. US companies (and other multinationals) that have established worldwide supply chains in China will suffer, as these factories are now stranded assets. There is a lot of this, so it is negative for the stock prices of these companies and thus the market as a whole.

- Longer term, supply chains will be relocated to other emerging Asia. So it's actually bullish for some assets in these countries, like real estate. Banks in places like Indonesia, Vietnam etc. would also benefit. I want to stress that this is longer term stuff. Shorter term, assets in EM will suffer, with the risk of a blowup in highly stressed ones like Turkey or Argentina.

- The next trade domino will be the EU. Since that area is already in secular stagnation, this could have serious consequences. A lot of the EU stock market is auto-based, and this would be the main target. If the Germans allow a fiscal stimulus, this could be managed. Don't bet on it.

The most important trading advice I can give is not to trade on stuff you don't have a strong view about. I felt that the deal was going to go through, but I knew I didn't have any insight that the market didn't already know. So I did not trade it. If I had shorted bonds, like I was thinking about a few posts ago https://thecommoditystrategist.blogspot.com/2019/04/long-time-no-post.html, I would already be out of pocket.

Monday, May 6, 2019

More on Tesla Bonds

Here's a link to a good article on TSLA bonds: https://seekingalpha.com/article/4244261-tesla-netflix-bonds-likely-smarter-bet-shares This will be a paywall for some of you. The article is about the capital structure of high yield companies: basically junk bonds do better than junk equity. I believe that this is widely studied and agreed with by academics.

The latest TSLA refinancing round went well, but I do not believe that is the end. Tesla has two problems:

1. Subsidies for electric cars have/are ending in several important markets.

2. Tesla's European competitors are launching similar products. They are doing this without a need for profitability. Germany is much like China. If the elite want something done, it gets done without regard to economics. Look at what happened to their electricity prices after they decided to invest in wind. This is bad for Mercedes/BMW/VW stockholders, but they don't count for much.

So the bonds are risky. I still believe that Tesla has technology worth the value of the bonds. The 8/25 bonds have rallied a point or so. I took a small position, and am going to watch for a place to add more.

The latest TSLA refinancing round went well, but I do not believe that is the end. Tesla has two problems:

1. Subsidies for electric cars have/are ending in several important markets.

2. Tesla's European competitors are launching similar products. They are doing this without a need for profitability. Germany is much like China. If the elite want something done, it gets done without regard to economics. Look at what happened to their electricity prices after they decided to invest in wind. This is bad for Mercedes/BMW/VW stockholders, but they don't count for much.

So the bonds are risky. I still believe that Tesla has technology worth the value of the bonds. The 8/25 bonds have rallied a point or so. I took a small position, and am going to watch for a place to add more.

Thursday, May 2, 2019

US Agriculture

The US ag markets will probably get a big kick up when (if?) a US - China deal is struck. How much depends on the type of deal. If it looks like a realistic deal that both sides can enforce, it will be major, not just for the ags but for all risk markets. OTOH, if it looks like something where the Chinese are biding for time until a Democrat takes office, not so much. I think it will be bullish.

Longer-term tho, US agriculture will have problems. Here's my list...

- The US is no longer the low cost producer. US farming methods are now widely disbursed, and labor and land costs are lower in much of the world.

- The bull case for ags was always that developing countries will transition to a high-protein, high-fat diet like the US. I am beginning to think this will not happen. The US diet is basically a northern European diet. That was OK when people lives were pretty much farming and warfare. No one should eat that kind of diet now, but at least the northern Europeans have genetic association with it. It's especially bad for everyone else. The diabetes rate in China is higher than in the US. So I do not think that the animal-intensive diet will go worldwide.

- Climate change!!!!! I have explicitly avoided mentioning the CC phrase in this blog. I'm averse to conflict, LOL. But here it matters. The increase in CO2 is contributing to a "greening" of the planet which is increasing ag yields worldwide. Maybe good for humanity, but bad for the markets.

Here's NASA's take: https://www.nasa.gov/feature/goddard/2016/carbon-dioxide-fertilization-greening-earth

How to play this. This is not a commodity market story. The real play will be in farmland. There are several farmland REITs that I am looking to short, the most obvious being FPI. But we have to wait till the China story resolves.

Longer-term tho, US agriculture will have problems. Here's my list...

- The US is no longer the low cost producer. US farming methods are now widely disbursed, and labor and land costs are lower in much of the world.

- The bull case for ags was always that developing countries will transition to a high-protein, high-fat diet like the US. I am beginning to think this will not happen. The US diet is basically a northern European diet. That was OK when people lives were pretty much farming and warfare. No one should eat that kind of diet now, but at least the northern Europeans have genetic association with it. It's especially bad for everyone else. The diabetes rate in China is higher than in the US. So I do not think that the animal-intensive diet will go worldwide.

- Climate change!!!!! I have explicitly avoided mentioning the CC phrase in this blog. I'm averse to conflict, LOL. But here it matters. The increase in CO2 is contributing to a "greening" of the planet which is increasing ag yields worldwide. Maybe good for humanity, but bad for the markets.

Here's NASA's take: https://www.nasa.gov/feature/goddard/2016/carbon-dioxide-fertilization-greening-earth

How to play this. This is not a commodity market story. The real play will be in farmland. There are several farmland REITs that I am looking to short, the most obvious being FPI. But we have to wait till the China story resolves.

Monday, April 29, 2019

Why is Inflation so Low?

The Phillips curve tradeoff of inflation vs. unemployment is a triumph of narrative over data. Here's a graph annually from 1960. If the Phillips curve had any validity, this would be an upward sloping series of dots, more or less.

Well it obviously is not. In fact there is a very low statistical significance here, certainly not enough to make policy on. For those years with less than 6% unemployment, there's no relationship at all. So why does everyone believe it?

Well it obviously is not. In fact there is a very low statistical significance here, certainly not enough to make policy on. For those years with less than 6% unemployment, there's no relationship at all. So why does everyone believe it?

Because the narrative is compelling. Common sense tells you that if labor is tight, workers will be able to demand higher wages. The problem with this argument is typical of economics; there are a lot of confounding variables that interact in unknown ways. They screw up the relationship.

If an economist asked a data scientist to look at the above chart, he would roll his eyes. Data people are used to looking at relationships that have actual power. Now I know that it is possible to construct models using lags and intermediate relationships that have greater explanatory power.

I call this "theory mining." The space of possible models is essentially infinite. So if you try enough things, you will come up with a theory that explains the past. The future; not so much.

My view is that demographics and social factors are all in the mix. There's not enough variation in the history to tease this out of the data, but it's my narrative. It's no coincidence that the one episode we had of actual high inflation since WWII was in the 70s, when the boomers were starting families and jobs. Now it's the opposite. We are going to have a continually aging population for several decades. Now I love old people, but they don't buy much stuff. Either they already have it, they are on fixed incomes, or they have moved on to other facets of their lives. There's a reason advertisers go after the 18 to 44 age bracket.

Of course this is not just happening in the US. The whole developed world and much of the emerging markets are in the same situation. So I expect the world central banks are going to have keep interest rates lowish for longerish.

That doesn't mean commodities prices will stay low. The world economy is still expanding, and there's not enough investment going into basic materials. One of these days that is going to matter.

Because the narrative is compelling. Common sense tells you that if labor is tight, workers will be able to demand higher wages. The problem with this argument is typical of economics; there are a lot of confounding variables that interact in unknown ways. They screw up the relationship.

If an economist asked a data scientist to look at the above chart, he would roll his eyes. Data people are used to looking at relationships that have actual power. Now I know that it is possible to construct models using lags and intermediate relationships that have greater explanatory power.

I call this "theory mining." The space of possible models is essentially infinite. So if you try enough things, you will come up with a theory that explains the past. The future; not so much.

My view is that demographics and social factors are all in the mix. There's not enough variation in the history to tease this out of the data, but it's my narrative. It's no coincidence that the one episode we had of actual high inflation since WWII was in the 70s, when the boomers were starting families and jobs. Now it's the opposite. We are going to have a continually aging population for several decades. Now I love old people, but they don't buy much stuff. Either they already have it, they are on fixed incomes, or they have moved on to other facets of their lives. There's a reason advertisers go after the 18 to 44 age bracket.

Of course this is not just happening in the US. The whole developed world and much of the emerging markets are in the same situation. So I expect the world central banks are going to have keep interest rates lowish for longerish.

That doesn't mean commodities prices will stay low. The world economy is still expanding, and there's not enough investment going into basic materials. One of these days that is going to matter.

Friday, April 26, 2019

Westinghouse Air Brake

I bought some Westinghouse Air Brake yesterday (WAB). It's a stock I l have been trading for awhile. Here's a link to a post I wrote on Seeking Alpha on it. LINK Note: this may have a paywall to some of you.

I like the US railroad story, particularly the two eastern RRs, CSX and NSC. The key part of the story is that many highways in this region are at full capacity. No more highways will be built. So RRs, which have extra capacity, should benefit. This is already happening as RR intermodal booms from the port of New York and on Florida east coast. This same story is true to a lesser extent on the west coast.

Wabtec recently bought GE's locomotive business. Wabtec and Caterpillar now produce a large majority of the world's diesel-electric motive power.

That market has been down for some time (why GE sold it). But I think the long run is great, not just in the US, but in EM as well. So I like Wabtec.

Risks:

- Company is now highly levered.

- New CEO is from GE. GE was a terrible company for many years.

- Precision railroading may reduce the number of locomotives needed.

For now this is a trading long. There's still enough skepticism about the situation, particularly the GE connection, to prevent a runaway market.

I like the US railroad story, particularly the two eastern RRs, CSX and NSC. The key part of the story is that many highways in this region are at full capacity. No more highways will be built. So RRs, which have extra capacity, should benefit. This is already happening as RR intermodal booms from the port of New York and on Florida east coast. This same story is true to a lesser extent on the west coast.

Wabtec recently bought GE's locomotive business. Wabtec and Caterpillar now produce a large majority of the world's diesel-electric motive power.

That market has been down for some time (why GE sold it). But I think the long run is great, not just in the US, but in EM as well. So I like Wabtec.

Risks:

- Company is now highly levered.

- New CEO is from GE. GE was a terrible company for many years.

- Precision railroading may reduce the number of locomotives needed.

For now this is a trading long. There's still enough skepticism about the situation, particularly the GE connection, to prevent a runaway market.

Wednesday, April 24, 2019

Tesla Bonds

It shows what people want to talk about. I write maybe 20 posts on commodities and get x page views. I write a post on Tesla and get 10x....

One reader mentioned that if I believe the situation in yesterday's post I should be buying Tesla bonds. My thesis was that Tesla has a lot of intellectual capital that is not counted on its books. So even if Tesla has to issue more equity to survive, the bonds should be money good. In fact, if Tesla was to go Chapter 11, it might be great for the bonds. You would get control of an undervalued asset. Just think of what Germany Inc. or China would be willing to pay for Tesla.

The bonds are yielding about 8.5%. Normally I only buy junk bonds when there is a scare catalyst, like a default. But I may start a position here.

One reader mentioned that if I believe the situation in yesterday's post I should be buying Tesla bonds. My thesis was that Tesla has a lot of intellectual capital that is not counted on its books. So even if Tesla has to issue more equity to survive, the bonds should be money good. In fact, if Tesla was to go Chapter 11, it might be great for the bonds. You would get control of an undervalued asset. Just think of what Germany Inc. or China would be willing to pay for Tesla.

The bonds are yielding about 8.5%. Normally I only buy junk bonds when there is a scare catalyst, like a default. But I may start a position here.

Tuesday, April 23, 2019

Tesla

As far as I'm concerned, the big news yesterday was Tesla's announcement that they have perfected self-driving enough to introduce it at the end of this year. If true, this is a revolutionary time frame. Many other observers are looking towards five to ten years.

I'm sceptical. A UBS analyst who went for a drive in it said that it required human intervention twice, even though the course was in good weather. So I'm not holding my breath.

One very big plus about Tesla that is mostly overlooked is that they design and build their own self driving chips. This is a major advantage. Their competitors buy NVDA gpu-based chips. These are slower and inherently less efficient. It's like the difference between mining bitcoin with an off-the-shelf chip vs. a custom made ASIC. I'm not sure how Tesla is going to monetize this, but there probably is a way.

That's why TSLA is such a complicated stock. Its intellectual capital is enormous; the ASIC chip is just the tip of the iceberg. OTOH, the company has had execution problems in its manufacturing operations. Maybe they should become a supplier to the rest of the industry. If they ever get to an oversold condition, maybe around $200, I'll buy it.

I'm sceptical. A UBS analyst who went for a drive in it said that it required human intervention twice, even though the course was in good weather. So I'm not holding my breath.

One very big plus about Tesla that is mostly overlooked is that they design and build their own self driving chips. This is a major advantage. Their competitors buy NVDA gpu-based chips. These are slower and inherently less efficient. It's like the difference between mining bitcoin with an off-the-shelf chip vs. a custom made ASIC. I'm not sure how Tesla is going to monetize this, but there probably is a way.

That's why TSLA is such a complicated stock. Its intellectual capital is enormous; the ASIC chip is just the tip of the iceberg. OTOH, the company has had execution problems in its manufacturing operations. Maybe they should become a supplier to the rest of the industry. If they ever get to an oversold condition, maybe around $200, I'll buy it.

Monday, April 22, 2019

Long time no post...

So here goes...

The oil long is working great. I've booked about 40% of it. It was the biggest trade I've had for awhile, so it's still pretty big.

Thinking of selling bonds. The fundamentals are there, but I prefer to enter on overbought/sold situations, and that's not there.

Also sticking with the eastern US railroads. These may be a little ahead of themselves now, but the long term is still great. I noticed that Mercedes Benz, one of the largest big rig manufacturers in the world, is giving up on truck platooning. They claim it doesn't make economic sense. This undercuts a long-term risk to railroad intermodal.

The oil long is working great. I've booked about 40% of it. It was the biggest trade I've had for awhile, so it's still pretty big.

Thinking of selling bonds. The fundamentals are there, but I prefer to enter on overbought/sold situations, and that's not there.

Also sticking with the eastern US railroads. These may be a little ahead of themselves now, but the long term is still great. I noticed that Mercedes Benz, one of the largest big rig manufacturers in the world, is giving up on truck platooning. They claim it doesn't make economic sense. This undercuts a long-term risk to railroad intermodal.

Friday, January 25, 2019

Why hasn't the Major Buy Occured

Back on 8/8/2018 I posted "Major Buy in the Materials Cycle?" The thesis was that the commodity markets were going to implode because of a growth slowdown in the commodity-intensive emerging markets (mostly China). This would provide a low risk window to load the boat in the materials sector. I guessed that this would take about six months.

Well, six months have come and gone. I have loaded the boat in oil (WTI). That trade was timed perfectly, and I am actually taking some off at this point. But we haven't seen the major commodity-wide selloff that I was hoping for. So outside of oil, I'm still only in opportunistic positions.

What has happened? For one, the market is thinking that the US and China will come to some sort of agreement. That is clearly in the best interests of both parties. So that's supporting prices. Also, there has been increased demand from countries such as India that have made up some of the difference.

Probably the most important thing is that people in the sector are thinking like me: the long run needs higher investment and that needs higher prices. So people are willing to accumulate inventory.

I'm sure most readers of this blog are acquainted with the "fat pitch" concept. Unlike in baseball, where you only get a limited number of pitches to look at, in investing the pitches keep coming. If you have to put up monthly numbers, maybe you have to swing at some to justify your management fees. I don't have this pressure anymore, so I can just sit back. That's pretty much where I am now.

Well, six months have come and gone. I have loaded the boat in oil (WTI). That trade was timed perfectly, and I am actually taking some off at this point. But we haven't seen the major commodity-wide selloff that I was hoping for. So outside of oil, I'm still only in opportunistic positions.

What has happened? For one, the market is thinking that the US and China will come to some sort of agreement. That is clearly in the best interests of both parties. So that's supporting prices. Also, there has been increased demand from countries such as India that have made up some of the difference.

Probably the most important thing is that people in the sector are thinking like me: the long run needs higher investment and that needs higher prices. So people are willing to accumulate inventory.

I'm sure most readers of this blog are acquainted with the "fat pitch" concept. Unlike in baseball, where you only get a limited number of pitches to look at, in investing the pitches keep coming. If you have to put up monthly numbers, maybe you have to swing at some to justify your management fees. I don't have this pressure anymore, so I can just sit back. That's pretty much where I am now.

Sunday, January 13, 2019

More on Bitcoin

Last November, I wrote my only post ever on Bitcoin. At the time I didn't have a market forecast, but I thought that there would be a ceiling on the market caused by large "foundational" holders using upmoves to monetize their assets. The Bitcoin market collapsed shortly after I wrote the post. Then in mid- December the market started to move up on light volume.

At the time I guesstimated that maybe 40% of the Bitcoin were held by the large owners ("Bitcoin billionaires"). Since then, a Bitcoin data analysis shop, Flipside Crypto, has estimated that the 1000 largest Bitcoin addresses control 85% of the Bitcoins! Flipside also says that some of these addresses have been inactive for years, but are now starting to reawaken. I don't know much about Flipside, but their analysis may have merit. They keep track of Bitcoin on the individual address level. During December, the percentage of coins trading in the top 100 addresses fell pretty sharply.

https://bitinfocharts.com/comparison/top100cap-btc.html#log&3m

If they are right, this may start moving up again. I'll keep a watch on it, although I will not trade the market.

Longer term, I continue to think that the future for all the crypto assets will depend on progress in making them more usable. Right now this doesn't look too promising. The Lightning Network is Bitcoin's hope for transaction expansion. But it has only had tepid usage so far. There are real concerns about its intra-day security. Ethereum got clogged up with just one crypto game, Crypto-Kitties. Probably more important, some of the crypto developers are cutting staff. It seems that a bull market was needed for their economic sustainability.

Finally, there may be a mathematical problem with the process all cryptos use to avoid "double spending". It's possible that all these processes are susceptible to certain kinds of hacks, such as 51% attacks. Recently a moderate size cryptocurrency, Ethereum Classic, experienced this. NOTE: this is not the Ethereum that most people know about. It's a smaller fork. So the whole idea may have inborn problems.

I usually say "time will tell" in cases like this. However, many basic questions of computer science have resisted proof for decades. For example P=NP and the security of RSA encryption. Easy to state; impossible to prove. So time may not tell.

At the time I guesstimated that maybe 40% of the Bitcoin were held by the large owners ("Bitcoin billionaires"). Since then, a Bitcoin data analysis shop, Flipside Crypto, has estimated that the 1000 largest Bitcoin addresses control 85% of the Bitcoins! Flipside also says that some of these addresses have been inactive for years, but are now starting to reawaken. I don't know much about Flipside, but their analysis may have merit. They keep track of Bitcoin on the individual address level. During December, the percentage of coins trading in the top 100 addresses fell pretty sharply.

https://bitinfocharts.com/comparison/top100cap-btc.html#log&3m

If they are right, this may start moving up again. I'll keep a watch on it, although I will not trade the market.

Longer term, I continue to think that the future for all the crypto assets will depend on progress in making them more usable. Right now this doesn't look too promising. The Lightning Network is Bitcoin's hope for transaction expansion. But it has only had tepid usage so far. There are real concerns about its intra-day security. Ethereum got clogged up with just one crypto game, Crypto-Kitties. Probably more important, some of the crypto developers are cutting staff. It seems that a bull market was needed for their economic sustainability.

Finally, there may be a mathematical problem with the process all cryptos use to avoid "double spending". It's possible that all these processes are susceptible to certain kinds of hacks, such as 51% attacks. Recently a moderate size cryptocurrency, Ethereum Classic, experienced this. NOTE: this is not the Ethereum that most people know about. It's a smaller fork. So the whole idea may have inborn problems.

I usually say "time will tell" in cases like this. However, many basic questions of computer science have resisted proof for decades. For example P=NP and the security of RSA encryption. Easy to state; impossible to prove. So time may not tell.

Tuesday, January 8, 2019

Update on Cocoa

A while back I mentioned that I was going to trade cocoa from the long side. I thought that arrivals from the Ivory Coast were going to be light for the first part of the season. There is really no crop problem; it's just one of timing. However, the market can get upset on simply that. In cocoa most of the speculators have no fundamental crop information. They just see the published numbers. When those look bullish, they buy.

It's getting a little late in the game for this. Rainfall in the cocoa zone has been close to average, so I really do not see a big fundamental move. We are at the top of a long held trading range. So if we break out, there could be a lot of technical buying. I'm hoping for that, and an eventual long->short.

It's getting a little late in the game for this. Rainfall in the cocoa zone has been close to average, so I really do not see a big fundamental move. We are at the top of a long held trading range. So if we break out, there could be a lot of technical buying. I'm hoping for that, and an eventual long->short.

Monday, January 7, 2019

More Traffic

There's been a big increase in traffic to this blog since my call on the bottom in oil prices on Dec 26. As of now, that was within a few pennies of the dead-ass bottom. That was pure luck. I'm a commodity strategist, not a tactician. Nonetheless, I have been trading these markets for many decades, and I guess I've learned a little about tactics as well.

So welcome to all the new readers. I am going to try to publish posts more frequently from now on. I started this blog as a way to describe my own trades. I know from experience that if you put things down on paper and invite others to read them, you have a forced discipline. Sloppy stuff gets called on the carpet.

I'll keep doing this. But I'll also give my thoughts on markets that I may not have a position in. Of course, I will make it clear whether I am just giving my opinion or actually have dollars on the line.

So here goes...

Vanadium. Long time readers know that I had a very big position in Vanadium miners starting in Jan 2018. The Vd price went up and is now coming down. Here's a chart of vanadium pentoxide.

BTW, the chart is from a junior miner, Prophecy Development Corp., which has a claim in Nevada USA.

The key to the market going forward is how large the speculative stocks of Vd were built up. In my experience, this kind of bull market, combined with media blabbering about future Vd flow batteries, is the kind of move that leads to large buildups. So it may take awhile to work them off.

However, they will be worked off, and the long term for Vd is good. China used to be a large producer (from steel slag from domestic iron ore) and a small consumer. Now it's a small producer (they are using iron ore from Australia/Brazil that has no Vd.) and a large consumer. So at some point this will be another good trade. I just dipped my toe into Large Resources. (LGO in Toronto). LGO is a Canadian company with a Vd mine in Brazil. I believe it's the best Vd mine in the world. So I'm looking to add to that, either on declines or on signs of stability in the Vd price. Right now it's a very small position.

So welcome to all the new readers. I am going to try to publish posts more frequently from now on. I started this blog as a way to describe my own trades. I know from experience that if you put things down on paper and invite others to read them, you have a forced discipline. Sloppy stuff gets called on the carpet.

I'll keep doing this. But I'll also give my thoughts on markets that I may not have a position in. Of course, I will make it clear whether I am just giving my opinion or actually have dollars on the line.

So here goes...

Vanadium. Long time readers know that I had a very big position in Vanadium miners starting in Jan 2018. The Vd price went up and is now coming down. Here's a chart of vanadium pentoxide.

BTW, the chart is from a junior miner, Prophecy Development Corp., which has a claim in Nevada USA.

The key to the market going forward is how large the speculative stocks of Vd were built up. In my experience, this kind of bull market, combined with media blabbering about future Vd flow batteries, is the kind of move that leads to large buildups. So it may take awhile to work them off.

However, they will be worked off, and the long term for Vd is good. China used to be a large producer (from steel slag from domestic iron ore) and a small consumer. Now it's a small producer (they are using iron ore from Australia/Brazil that has no Vd.) and a large consumer. So at some point this will be another good trade. I just dipped my toe into Large Resources. (LGO in Toronto). LGO is a Canadian company with a Vd mine in Brazil. I believe it's the best Vd mine in the world. So I'm looking to add to that, either on declines or on signs of stability in the Vd price. Right now it's a very small position.

Wednesday, January 2, 2019

Oil Econometrics

Whenever I make a large trade I always develop a statistical model for it. I find that gives me a framework to trade around. Now, models are not always statistically good, and there may be reasons I don't trust them anyway. But they are a first step. Here's how I went about the oil model.

My simplist framework is this. First I deflate the price. then I form a moving average of the deflated price. I then estimate a model using the price ten years ago and time as independent variables. So it looks like this:

log(defPrice) = a + b * log(MovAvg(defPrice[-10]) + c * time

The -10 term is for mean reversion. Time is there because most commodities have secular trends in price. For most the trend is downward; commodities are getting cheaper relative to services etc. For a few the trend is upward, probably because of increasing difficulty of extraction.

Oil is one that has had an increasing trend. In the model, I manually stopped the trend five years ago. This is due to a new technology, fracking, that has somewhat changed the game.

Using monthly data, the oil model is surprisingly accurate. It's R-squared is about 85%. All the other diagnostics (about 20 of them) are also good. For example, here's a plot of the residuals versus pure normality:

This is fairly good. The residuals are pretty much normally distributed, although they miss on the upper tail. That doesn't bother me. There's a lot of evidence that liquid asset prices have fat tails, and in commodities the "fat" is usually on the upside.

Forecast for spot Brent...

Assuming inflation at 2% and the $US unchanged,

the price will be 64% higher in ten years.

Now that may not seem like a big move. I have found however, that a commodity rarely takes the full ten years to get to equilibrium. More like two or three.

For shorter term (1 - 3 years) forecasts, you need to input data on supply/demand/capacity. That's for another post.

My simplist framework is this. First I deflate the price. then I form a moving average of the deflated price. I then estimate a model using the price ten years ago and time as independent variables. So it looks like this:

log(defPrice) = a + b * log(MovAvg(defPrice[-10]) + c * time

The -10 term is for mean reversion. Time is there because most commodities have secular trends in price. For most the trend is downward; commodities are getting cheaper relative to services etc. For a few the trend is upward, probably because of increasing difficulty of extraction.

Oil is one that has had an increasing trend. In the model, I manually stopped the trend five years ago. This is due to a new technology, fracking, that has somewhat changed the game.

Using monthly data, the oil model is surprisingly accurate. It's R-squared is about 85%. All the other diagnostics (about 20 of them) are also good. For example, here's a plot of the residuals versus pure normality:

This is fairly good. The residuals are pretty much normally distributed, although they miss on the upper tail. That doesn't bother me. There's a lot of evidence that liquid asset prices have fat tails, and in commodities the "fat" is usually on the upside.

Forecast for spot Brent...

Assuming inflation at 2% and the $US unchanged,

the price will be 64% higher in ten years.

Now that may not seem like a big move. I have found however, that a commodity rarely takes the full ten years to get to equilibrium. More like two or three.

For shorter term (1 - 3 years) forecasts, you need to input data on supply/demand/capacity. That's for another post.

Subscribe to:

Posts (Atom)