POST 3

A theme one often hears in the commodity markets is the coming shortage of arable land and food supplies. The argument goes like this: World population continues to increase. Additionally, the exploding middle class in emerging markets (EM) like China and India now have the income to shift from a traditional diet to a developed market (DM) diet high in meat, fats and sweets. (More accurately that’s really a northern European/US diet rather than full DM). In 2014 people in EM only consumed 44% of the meat per capita as DM. Meat takes much larger agricultural resources per pound than the traditional diets. Meanwhile new agricultural land is limited in extent and marginal in productivity. Yields per acre are still increasing, but at a slower rate. This will get worse as most of the easy gains have been made. Climate change may accentuate the problem.

I believe the above argument is wrong. It is a classic case of narrative vs. data. The numbers simply do not support the argument. In fact, one could make just as strong a case for a chronic agriculture oversupply, especially if the political supports for products like ethanol are eliminated. I won’t make that case, but I will debunk the shortage.

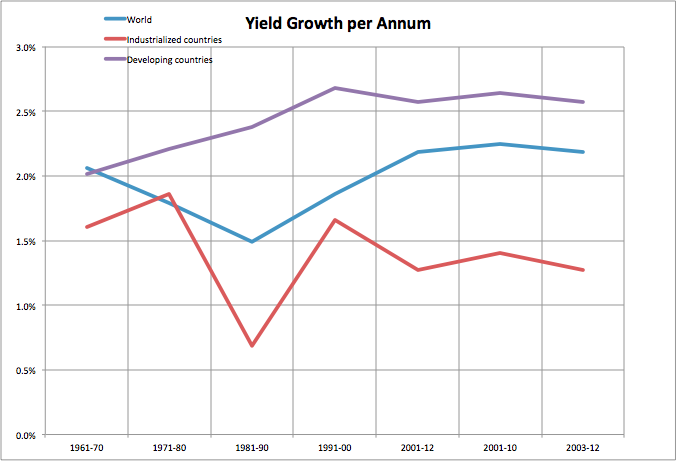

First let’s look at agricultural supply. It is true that the growth in yield per acre in the developed nations have decelerated to under 1% per year (although still increasing). But the same is not true in EM. Here’s a graph of yield per acre:

Note how total world yields increases have been remarkably stable for a very long time, except for the droughts in N. America in the 1980s. EM yields are still rising at over 2.5% per year. Combined with a small (about 0.2%) increase in land under cultivation, this will be enough to comfortably feed the world’s increasing population. Of course there are risks. Climate change may decrease (or increase) yields. War and general geopolitics may take land out of cultivation. Anti-technology advocates may restrict improvements in farming practices. But the base case is for continuing growth in food production.

Now let’s look at the demand side. A key fact here is that the demographic bust well known in developed economies has spread to EM. The United Nations predicts that world population will grow by only 0.9% per annum in the next 20 years. After that they predict a slow decline towards zero population growth. Note that this is an extremely important statistic for many industries besides food.

Second, there is good reason to believe that the EM population will never consume a northern European-US style diet. This may come as a surprise to many, but the diabetes problem in China is worse than in the US. According to a 2013 AMA report, 11.6% of Chinese adults are diabetic (vs. 11.3% in the US). Additionally, 40% of 18-to-29-year-olds in China are on the verge of developing the disease. This is a result of changes in diet and physical activity. It is taking place with meat, fat and overall calorie consumption levels that are far lower than in the US, and it possibly has a genetic component. The situation in India and southern Asia is progressing along the same lines but at an earlier stage.

I believe this will play itself out similarly to smoking. Fifteen years ago, China was considered the big growth market for tobacco. The government launched a spate of anti-smoking measures, and the tide is now turning. As time goes on, we will likely see a stream of healthier diet initiatives, and the tide of increasing meat consumption will also recede.

As much I dislike arguments from authority, I will point out that the USDA agrees with me. Its price forecasts for the major US agricultural products like corn, wheat and soybeans are pretty much flat for the next ten years.

It’s important to stress that I am talking about overall agricultural supply and demand. There will be many sectors of the market that will do very well. I especially like more expensive and reasonably healthy sectors like fruit, tree nuts and farmed fish. As an example, many Chinese have recently developed a taste for pecans, almost all of which are grown in the US. This has led to significant price increases and substantial profits for the US industry.

I’ll get to the specific investments in the sector that I own in future posts.

No comments:

Post a Comment

Comments are welcome, although I can't promise to answer every question.