Undervaluation The ten-year graphs on this site forecast that nickel will double in real terms in ten years. That's a pretty good starting point. Nickel is the most undervalued metal I follow. BTW, there is a good reason for this. Back a few years ago, when China was frantically buying every metal in sight, Indonesia enacted an embargo on nickel ore exports. Their objective was to force local processing of the ore. Because many believed that Indonesia could not build the necessary processing facilities quickly enough, this created a panic in the market. Nickel went to absurdly high prices. This led to more production, and the typical commodity "cobweb" ensued. I think we are now at the opposite end of the cycle.

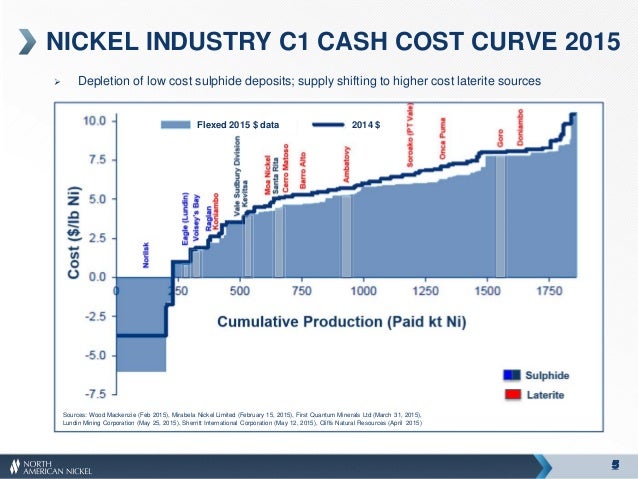

Nickel now sells for about $4 per lb. The graph below gives the cost curve. Most production is now losing money. BTW, the negative costs for Norislk (NILSY) is not an error. Norilsk produces so much coproduct metals that it more than covers their production costs. More on that later.

The fact that these miners are losing money does not mean they will shut down production immediately. Current prices may well cover their cash production costs. Also, some production is going to be subsidised. For example, France said last month that it would subsidise the nickel industry in New Caledonia, which had previously been expected to reduce production. Another issue is that the value of the Indonesian Rupiah has fallen by about half. This reduces the cost curve.

Nonetheless, the main thrust of this blog is to think strategically. All the above risks are short to intermediate term. In due time production will be shut down, and prices will rise. The remaining producers wind up doing very well. This is a three year trade.

So how to play this. Normally for longer term trades, I like to invest in the equity or debt of the lowest cost tradable producer. That would be Norilsk. For more on Norilsk's fundamentals, see the excellent Seeking Alpha article

http://seekingalpha.com/article/3940446-norilsk-nickel-worlds-largest-nickel-palladium-producer-significantly-undervalued

My numbers are slightly different from his, but only marginally. Also note that Norilsk also produces other metals, particularly copper and palladium. These revenues combined are actually larger than from nickel. I am a little bullish on palladium and a little bearish on copper.

In this case, however, I also bought LME nickel. The total return from this I estimate at 10% - 15% per year unlevered (I am unlevered). It's also easily tradable. More important, it does not have the Russian country risk. Now I personally feel that the Russian situation is not as bad as the market thinks, and its market is undervalued. But I could easily be wrong here. So keep that in mind if you follow me into Norilsk.

Hei,

ReplyDeleteLove the site. For a 'quant', I reckon your feel, your intuition for socio-politics is rather solid. So much better than so many pundits whose sectarian bias seems to colour far too much analysis.

Am a long-suffering shareholder of Sherritt International here which I bought for the lateritic project Ambatovy in Madagascar as well as a play levered to the inevitable thawing of relations between the USA and Cuba. Sherritt has oil, nickel and energy assets in Cuba.

Clearly, I underestimated that extent of the collapse in the relevant commodity prices but reckon that the junk-rated Sherritt corporate debt will survive and will pay in relative terms handsomely. Diversifying into Norilsk strikes me as a good idea, especially I expect the Crimean issue to gradually resolve itself without significant further drama.

Must admit that I tend to buck against anything that relies on a forecast longer than 9 to 12 months. The only forecasting in economics that works with any kind of useful consistency beyond a few months is US yield curve recession recasting and even that appears to work only for the USA.

It would be interesting to acquire longer time series and test the forward ten year return model with historic out-of-sample forecasts. I am guessing/assuming that that has not been done already.

There are certainly a number of ways of motivating the model. Although thinking about the historic path of oil prices, I sometimes wonder if a 10 year return horizon will always be sufficiently long.

I could ramble on. Thanks for the blog; as an overseas oil and gas exploration specialized investor, this blog is the best find I have made in a long time. h/t to Ben Bernanke.

10^3 thanks -Erik

Thanks for the kind words. If you really feel that the Russian geopolitical situations will improve, all Russian assets are a screaming buy.

ReplyDeleteYes. That said, stylistically, Putin is tough to swallow on occasion.

DeleteMoreover, regardless of the broader geopolitical context, economic property rights in Russia are far from secure. I suppose that means drilling down and figuring out which assets are safe from an arbitrary taking and which are not.

Hmm.....